DEAR SOPHIA,

THIS IS HISTORY IN THE MAKING. THE PETRODOLLAR BECAME THE UNDERPINNING OF THE AMERICAN FINANCIAL SYSTEM IN 1971 – NOT 1974. BUT THAT’S OK – THEY CAN SAY ITS 1974. IT IS ABSOLUTELY IMPERATIVE THAT THE DOLLAR REMAIN KING FOR PETRODOLLARS AND ALL WORLDWIDE COMMERCE. IF THE DOLLAR IS DETHRONED, THERE IS ABSOLUTELY NO REASON FOR THE AMERICAN POWER OF ANY KIND TO BE RELEVANT. REGARDLESS OF WHAT THE TALKING HEADS SAY ABOUT ENDLESS WARS, THE PRESIDENT HAS ONE OVERRIDING PRIORITY IN CONJUNCTION WITH HIS OATH OF OFFICE AND THAT IS TO MAINTAIN AMERICAN SUPREMACY OVER THE GLOBAL FINANCIAL SYSTEM. IF HE DOES NOT DO THAT, THEN HE IS RELINQUISHING AMERICAN POWER AND EVERY FINANCIAL, POLITICAL, MILITARY INTEREST WILL REACT TO PRESERVE SUPREMACY. THEREFORE, IF I WAS A BETTING MAN, THERE WILL BE BOOTS ON THE GROUND ON KARGE ISLAND AND THE PRESIDENT WILL HAVE NO OTHER OPTION BUT TO ENFORCE AMERICAN SUPREMACY ON THE PETRODOLLAR MARKET. READ THE ARTICLE BELOW. EVERY PRESIDENT SINCE FDR HAS UNDERSTOOD THE ABSOLUTELY PARAMOUNT INTEREST OF THE MIDDLE EAST TO THE UNITED STATES. IN A PARADOX, IT IS ACTUALLY BETTER POLICY TO IMPORT MORE OIL AND LEAVE OURS IN THE GROUND TO IMPOSE MORE FINANCIAL SUPREMACY ON THE PETRODOLLAR SYSTEM.

143

LOVE,

DAD

How the Iranian war may lead to the last days of the petrodollar

Provided by Dow Jones Mar 25, 2026, 5:16:00 AM

By Jules Rimmer

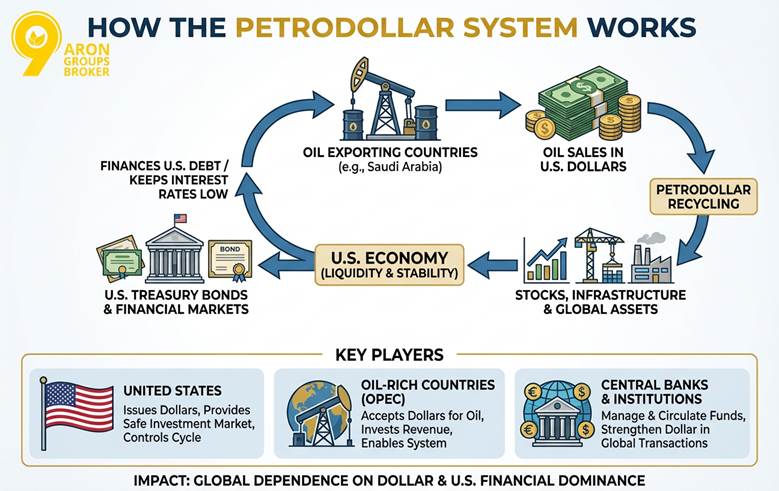

Accumulating dollars to pay for energy has underpinned the U.S. currency for decades

Oil exporting nations have typically recycled their petrodollars into U.S. Treasurys

One unintended consequence of the Middle East conflict may be the end of what is called the petrodollar regime.

The world saves in dollars largely because it pays for its energy in dollars. If the disruption caused by the effective closure of the Strait of Hormuz leads to major economies trading oil in other currencies then this could seriously undermine the dollar’s hegemony in central bank reserves and global trade.

This warning was sounded by Deutsche Bank strategist, Mallika Sachdeva in a special report published Tuesday, subtitled “the perfect storm for the petrodollar.” Deutsche Bank’s views on the U.S. currency caused a controversy back in January when a note from its head of forex strategy, George Saravelos, provoked the ire of Treasury Secretary Scott Bessent.

If Bessent disapproved of those views then he’s unlikely to look more favorably on the latest research in which Sachdeva argues that the dollar’s dominance in cross-border commerce is arguably built on the petrodollar, and right now, these are flimsy foundations.

Oil is quoted in dollars, invoiced in dollars and settled in dollars, Sachdeva points out, and this practice dates back to an agreement struck between the U.S. and the Saudis back in 1974. The Desert Kingdom agreed to invest its trade surpluses in dollar assets in return for U.S. security guarantees, she writes, and those assets were generally U.S. Treasurys.

The dominance of the dollar in cross-border trade has a lot to do with the petrodollar.

As energy exporters accumulated dollar reserves, this allowed the U.S. to borrow extensively and cheaply, what former French president Valery Giscard d’Estaing called its “exorbitant privilege.”

However, Sachdeva contends, the world is changing and most of the oil produced in the Middle East is sold to Asia, not America, which is now a net exporter itself. Sanctioned Iranian and Russian oil (producing between them roughly 13 million barrels of crude daily, around 14% of global consumption) has been trading “off the dollar rails,” as Sachdeva puts it, for some time. The Saudis have been experimenting, she observes, with forms of non-dollar payment such as the Project mBridge infrastructure, using a central bank digital currency.

There were already signs of instability to petrodollar foundations: Saudi Arabia sells four times as much oil to China now as to the U.S.

Sachdeva is concerned that the regional escalation of the Gulf conflict may end up challenging assumptions about the security umbrella the U.S. provides, and may oblige some of these countries to unwind their savings in foreign assets. For example, Sachdeva notes that there are reported instances in the last few weeks of tankers being guaranteed safe transit through the strait should the payments be denominated in yuan (USDCNY).

Sachdeva writes: “The conflict could be remembered as a key catalyst for erosion in petrodollar dominance and the beginnings of the petroyuan.”

A subsidiary consideration cited by Sachdeva is the possibility that as the world reduces its dependence on fossil fuels, perhaps to domestically available fuels, renewable energy and nuclear power, so the necessity of holding dollars may be reduced accordingly. “A world that becomes self-sufficient in defence and energy could also be a world that holds less dollar reserves.”

The U.S. dollar index DXY has edged up 1% this year, with the greenback not getting its typical safe-haven bid as investors expect price in more rate hikes from foreign central banks including the European Central Bank than they expect from the U.S.

-Jules Rimmer